Overview

TypeHNI Credit CardReward Rate4.8% to 25%Annual Fee30,000+GSTBest forHigh Value SpendsUSPAirline/hotel transfer partners

Due to the high joining fee, the Magnus Burgundy Credit Card is specifically designed for high-value spenders who are willing to invest some time to explore its airline and hotel transfer partners to maximize the point value.

Fees

Joining Fee30,000 INR+GSTWelcome Benefit5,000 INR Yatra VoucherRenewal Fee30,000 INR+GSTRenewal BenefitNilRenewal Fee waiverOn spending >30 lakhs

- Spend requirement for annual/renewal fee waiver will exclude spends done on: Insurance, Gold & Fuel

- It’s funny when you get only 5K INR voucher while the joining fee is ~35K INR (with GST).

But if you know the value of airmiles or hotel loyalty points, you would close your eyes and go for it.

The Axis Bank Magnus Burgundy Credit Card comes in a light-weight metal form factor and primarily operates on the Mastercard platform.

Interestingly, the bank has chosen not to include the word “Burgundy” anywhere on the card’s design.

As a result, it’s impossible to differentiate between the regular Magnus and the Magnus Burgundy solely based on appearance.

Rewards

SPEND TYPEREWARDSREWARD RATE

(EDGE REWARDS PORTAL)REWARD RATE

(POINTS TRANSFER at 5:4)Regular Spend12 RP / 200 INR1.2%4.8%Axis Travel Edge Portal (5X)60 RP / 200 INR 6%24%

The earn rate of Edge Rewards on regular Magnus & Magnus for Burgundy are same, however, because of the difference in points transfer ratio (5:2 for Magnus / 5:4 for Magnus Burgundy), it makes a world of difference, like 100% more value to be precise.

Exclusions for Rewards:

- Rent (Capped at 50K INR a month)

- Wallet, Utilities & Gov. Spends

- Insurance, Gold/Jewellery

- Fuel

Accelerated Rewards

- On Spends of >1.5L a month: Get 35 points / 200 INR (~14%)

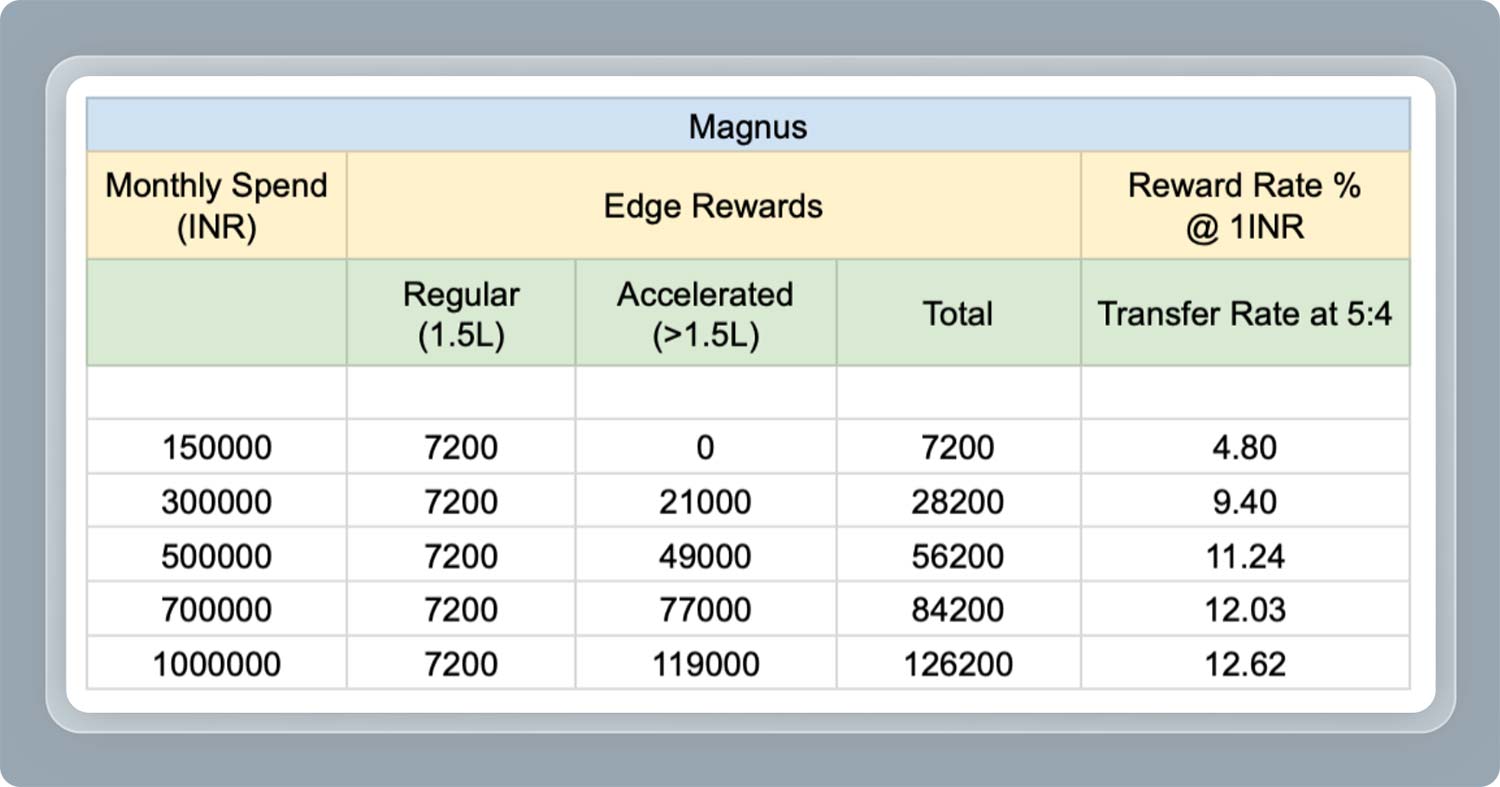

Magnus Burgundy is an amazing credit card for high spenders as its reward rate beats any card in any bank in the “world”, especially when “monthly” spends go up.

You get 14% return for spends over 1.5L INR in a month. But realistically, here’s how the numbers look like on average, as first 1.5L spend gives only 4.8% return.

As you can see, ~3L monthly spend on an average is the sweet spot to get close to 10% reward rate.

To give a perspective of how lucrative it is, HDFC Infinia used to offer the highest reward rate for very many years, which is 3.3% on regular spends.

On top of that, if you move the points to Accor, then it’s 1.8X the value, which is a sweet 18% return on day-to-spends.

5X on Travel Edge

- Earn 60 points / 200 INR (~24% as miles) upto 2L spends a month

- Earn 35 points / 200 INR (~14% as miles) beyond 2L spends a month

While 5X Rewards on Edge Rewards is good in a way, do note that dealing with Travel Edge portal is not an easy affair.

While 5X on travel edge is good, especially for flights, HDFC Infinia gives 33% return on smartbuy hotel bookings.

Redemption

- Redeem Edge Rewards to points/miles at 5:4 ratio

- Max up-to 10L points a calendar Year: 2L to Group A & 8L to Group B

GROUP AGROUP BAccor (Hotels)ITC (Hotels)Marriott (Hotels)IHG (Hotels)Wyndham (Hotels)Qantas AirwaysAir CanadaAir IndiaQatar AirwaysAir FranceUnited AirlinesSpice JetSingapore AirlinesAir AsiaTurkish AirlinesThai AirwaysJapan AirlinesEthiopian AirlinesEtihad Airways

If you’re wondering where to redeem, Accor Hotels (1.8 INR per Accor ALL Point) in Group A & ITC (1 INR per ITC Green point) in Group B are the safe & popular partners.

If you’re looking for airline partners, Air Canada, Singapore Airlines and Qatar are the next best.

But be aware that airline partners are risky as they tend to devalue miles overnight and you might end up sitting on ~50% lower value, just like how I’m sitting on few lakh miles with United Airlines.

Airport Lounge Access

ACCESS TYPEVIALIMITGUEST ACCESSDomestic Lounge AccessVisa / MastercardUnlimited4International Lounge Access (Primary)Priority PassUnlimited4

Guest access is a good one to have and it is limited to 4 per “calendar year” which is decent but 8 as before would have been lot better.

Note: With effect from 1st May 2024, the airport lounge benefits (domestic only) are available after spending 50K INR in the past 3 calendar months. This is cruel for a card of this grade.

Forex Markup Fee

- Foreign Currency Markup Fee: 2%+GST = 2.4%

- Net Return: Rewards – Markup Fee = 4.8% – 2.4% = ~2.4%

2.4% gain on forex spends is a very good return on spend in the industry. On top of it, if your monthly spends are higher, then it’s undoubtedly the best credit card for forex spends.

Comments (0)

No comments yet. Be the first to start the conversation!

Leave a Reply